Wall Street closes at a record for the first time since end of January

Introduction & Market Context

KBC Group (BR:KBC) showcased strong financial results in its Q4 and FY 2025 presentation released on February 12, 2026, with the Belgian bank-insurance group reporting significant growth across key metrics. The company’s stock responded positively to the results, rising 0.79% to €120.75 in morning trading.

The presentation highlighted KBC’s successful execution of its integrated bank-insurance strategy and digital-first approach, which have contributed to substantial improvements in profitability, efficiency, and customer engagement. Against a backdrop of economic challenges, KBC has leveraged its diversified business model to deliver robust performance.

Quarterly Performance Highlights

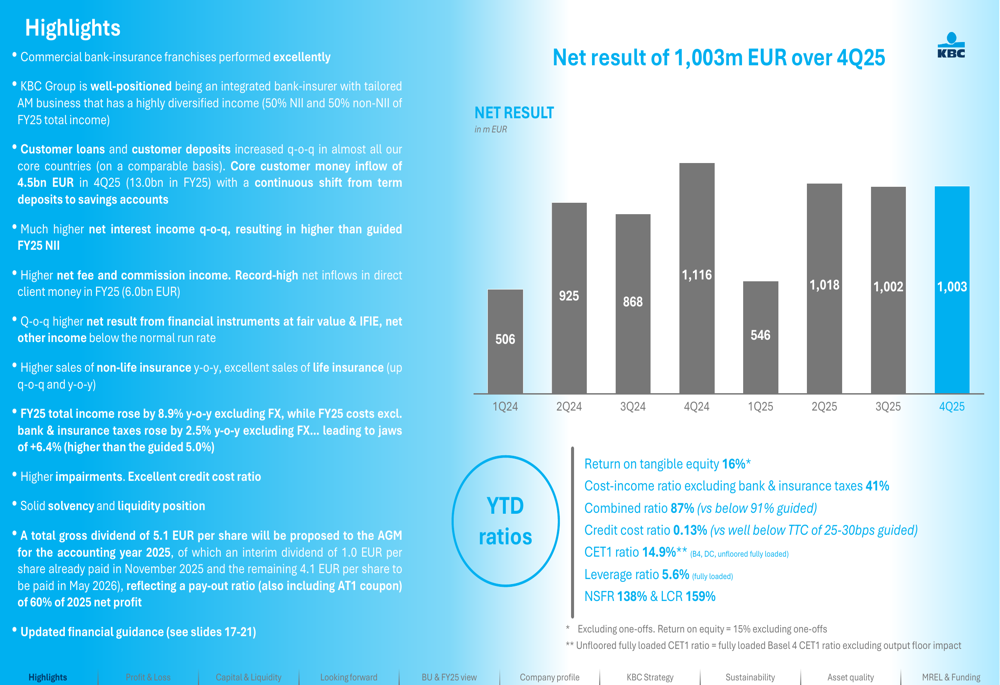

KBC reported a Q4 2025 net result of €1,003 million, nearly double the €506 million recorded in Q1 2024. For the full year 2025, total income grew by 8.9% year-over-year (excluding FX effects), demonstrating the strength of the group’s commercial franchises across its markets.

As shown in the following summary of key performance indicators, KBC achieved impressive results across multiple metrics:

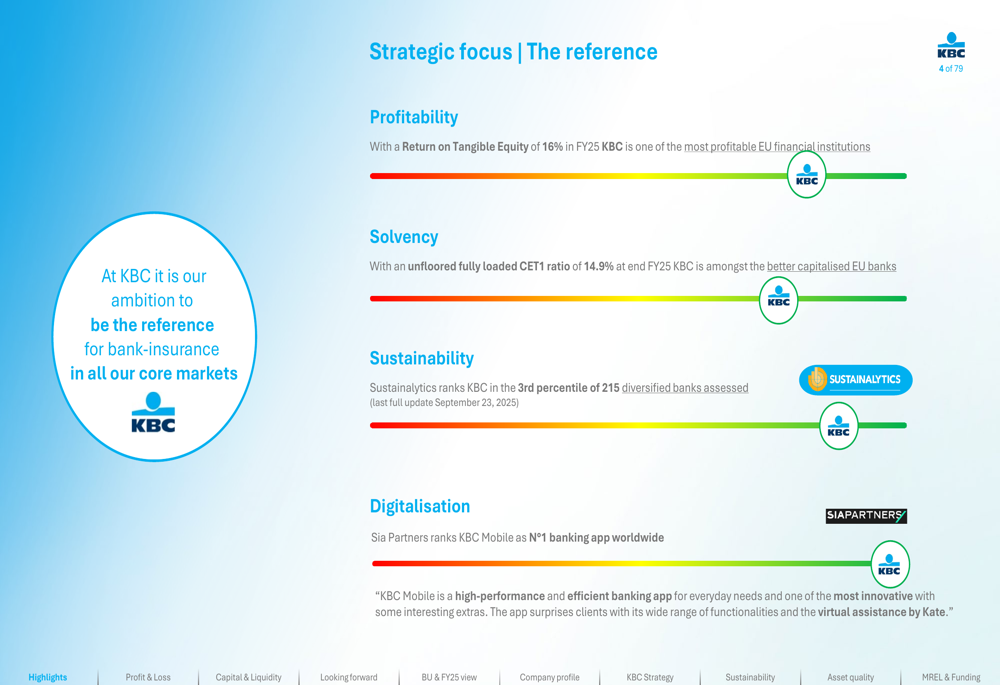

The bank’s return on tangible equity reached 16%, while the cost-income ratio improved to 41%, reflecting enhanced operational efficiency. The combined ratio for insurance operations stood at 87%, indicating solid underwriting performance. KBC maintained strong capital and liquidity positions with a CET1 ratio of 14.9% and liquidity coverage ratio of 159%.

CEO Johan Thijs emphasized the company’s operational excellence during the earnings call, stating, "The machine has been firing on all its cylinders." He particularly highlighted the benefits of AI integration through the company’s digital assistant KATE.

Detailed Financial Analysis

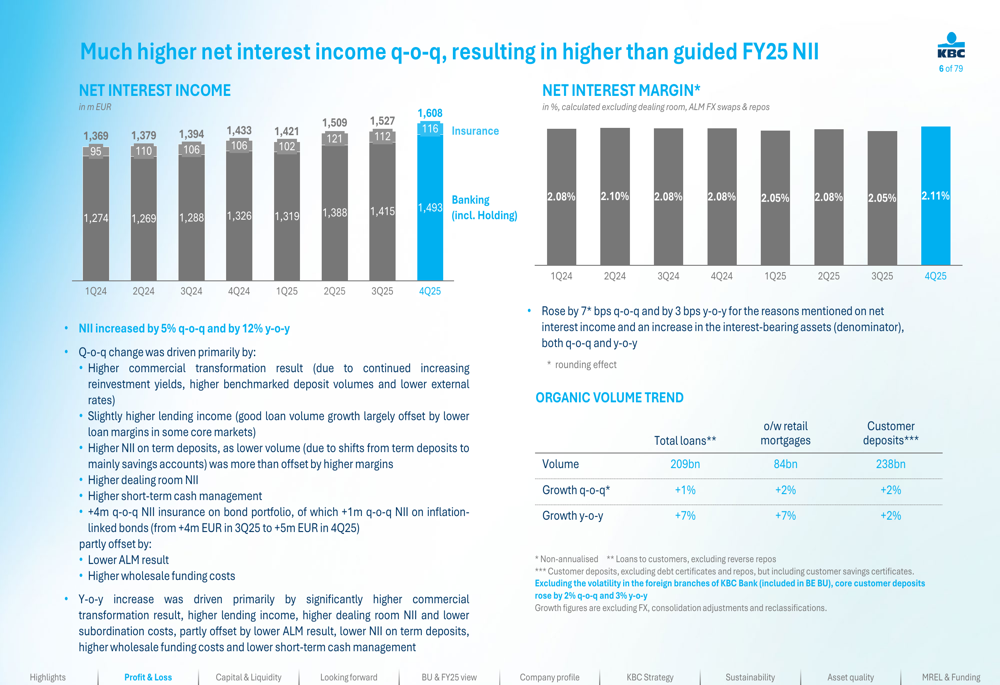

Net interest income showed consistent growth throughout 2025, exceeding the company’s guidance. This was supported by higher loan volumes, which increased 7% year-over-year to €209 billion, and customer deposits, which grew 2% to €238 billion.

The following chart illustrates the positive trend in net interest income and margin:

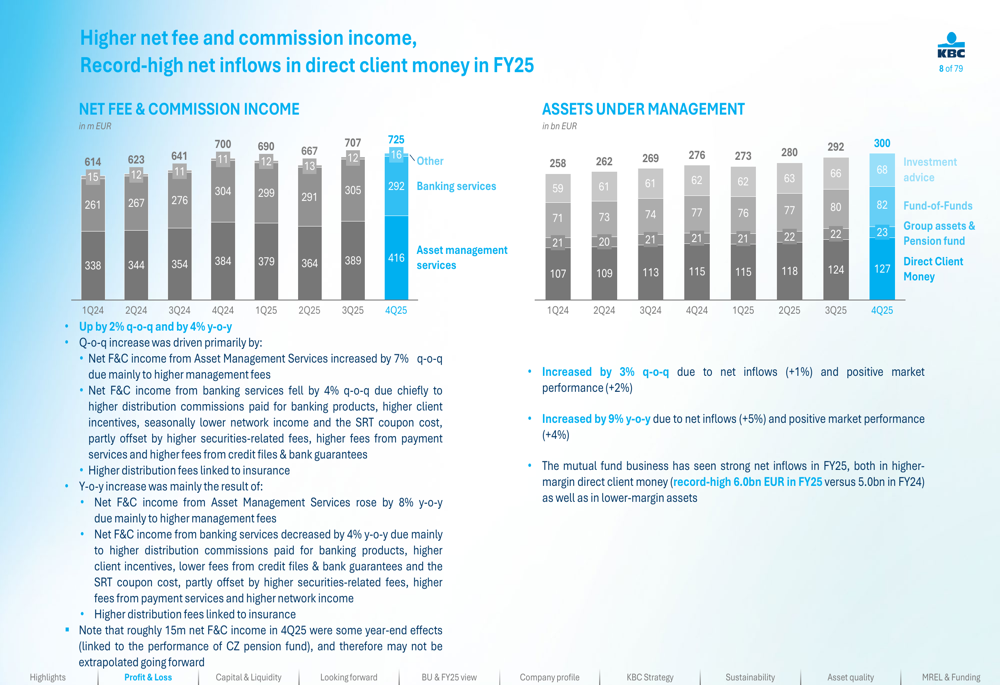

Fee and commission income also performed strongly, increasing from €614 million in Q1 2024 to €725 million in Q4 2025. This growth was primarily driven by asset management services and banking services. Assets under management reached €300 billion by the end of 2025, up from €258 billion in Q1 2024.

The composition and growth of fee income is detailed in this chart:

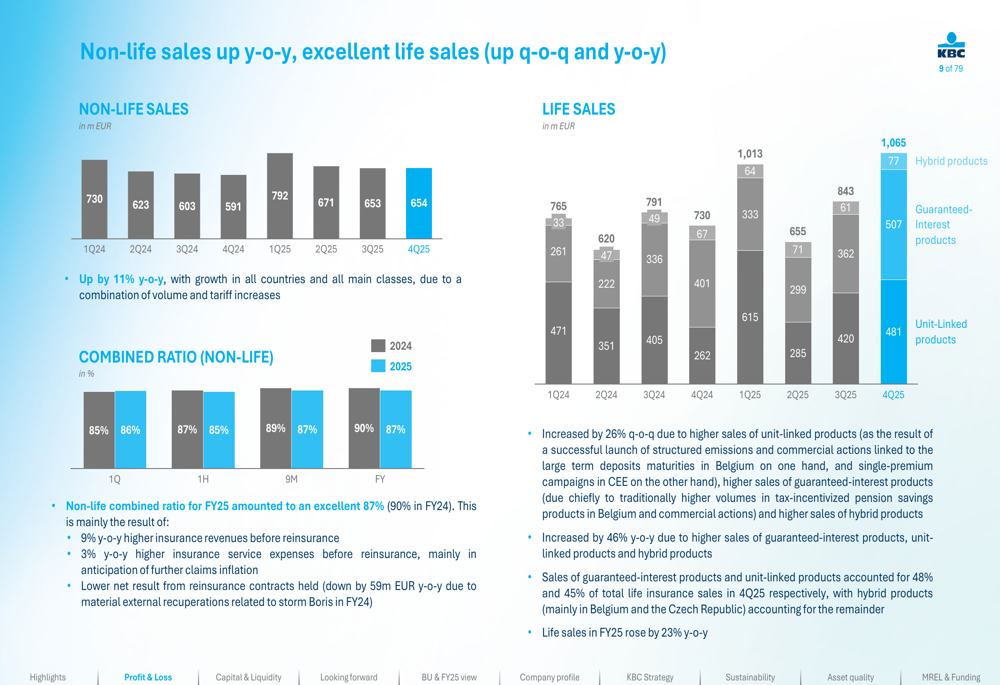

KBC’s insurance business continued to deliver solid results, with non-life sales up 9% year-over-year and life insurance sales increasing by 23%. The company saw growth across all countries and main insurance classes, contributing to the diversification of income streams.

The insurance sales performance is illustrated below:

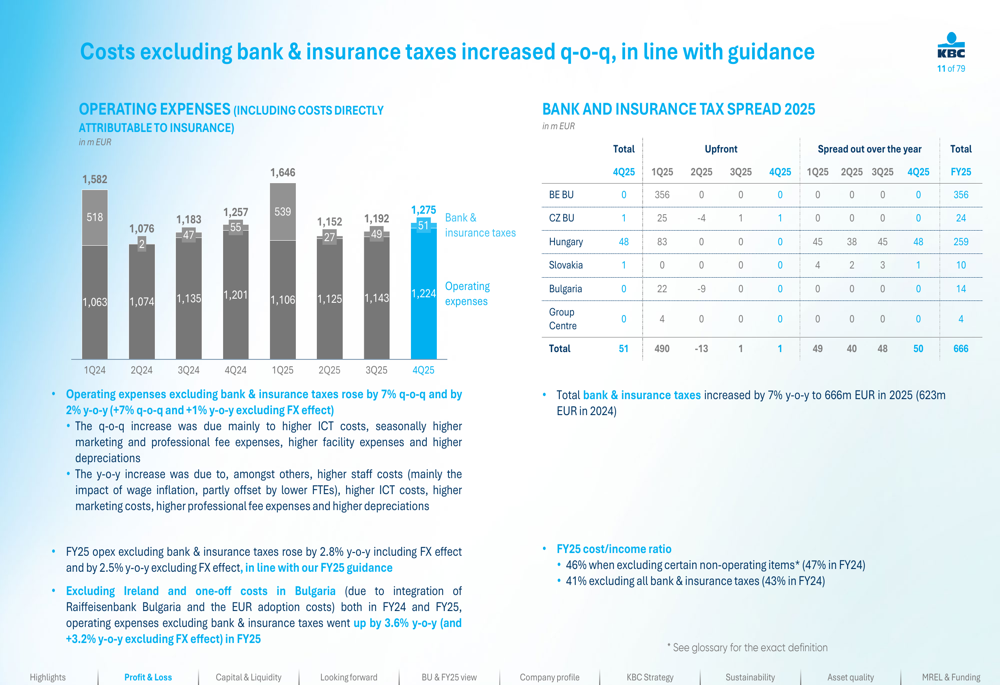

Cost management remained a priority for KBC, with operating expenses excluding bank and insurance taxes rising by just 2% year-over-year, despite inflationary pressures. This disciplined approach to costs, combined with growing income, led to an improved cost-income ratio of 41% when excluding bank and insurance taxes.

The following chart shows the evolution of operating expenses:

Strategic Initiatives

KBC’s strategic focus continues to center on three key pillars: its integrated bank-insurance model, digital-first approach, and embedded sustainability strategy. The company’s digital assistant KATE has become a cornerstone of its customer engagement strategy, with 6 million users now interacting with the AI-powered tool.

The bank’s digital leadership was recognized by Sia Partners, which ranked KBC Mobile as the number one banking app worldwide. KATE’s autonomy rates have reached impressive levels: 82% in Belgium and 69% in the Czech Republic, indicating the AI assistant’s growing capability to handle customer inquiries independently.

In terms of sustainability, KBC was ranked in the 3rd percentile of 215 diversified banks assessed by Sustainalytics in September 2025, positioning the company as a leader in environmental, social, and governance (ESG) practices.

Forward-Looking Statements

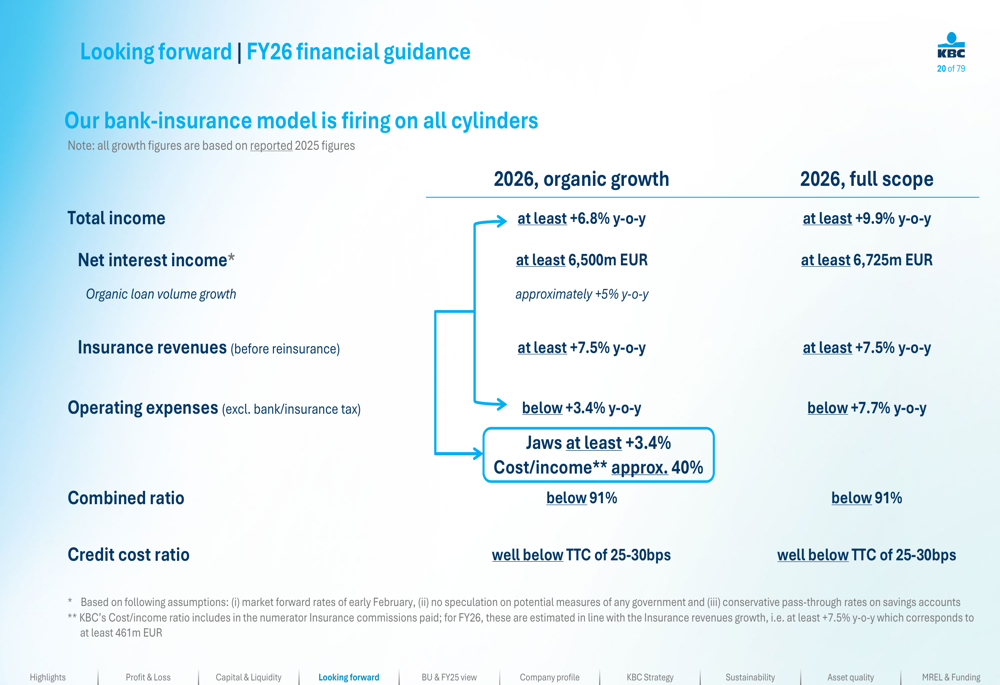

Looking ahead, KBC provided ambitious guidance for FY 2026 and beyond. For 2026, the company expects total income to grow by at least 6.8% organically (9.9% including acquisitions), with net interest income projected to reach at least €6,725 million on a full-scope basis.

The company aims to maintain positive jaws of at least 3.4% (income growth exceeding cost growth) and further improve its cost-income ratio to approximately 40%.

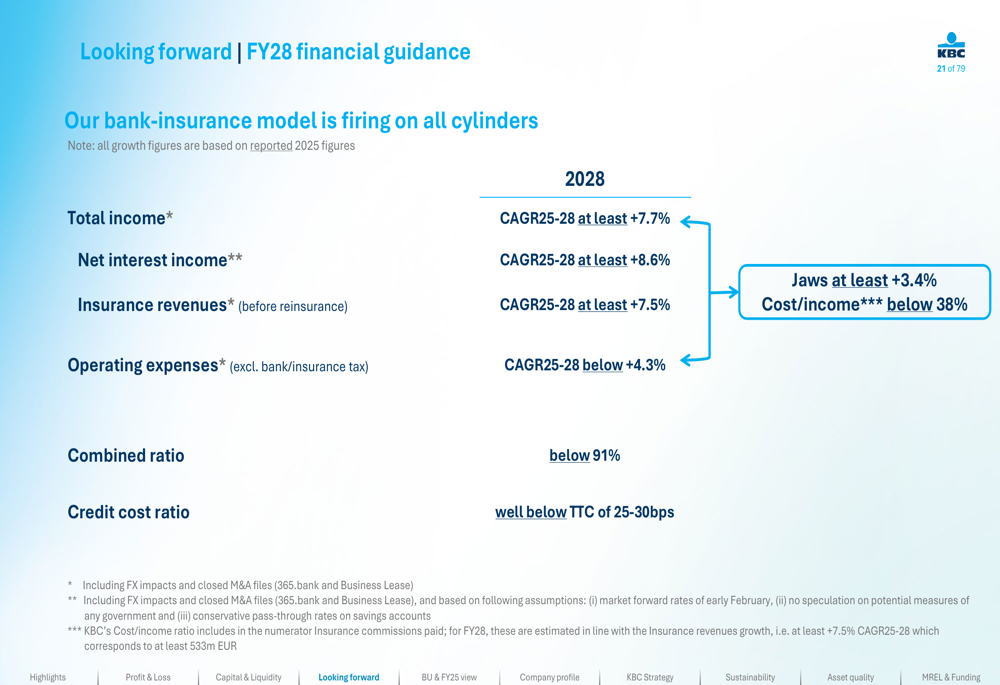

For the longer term, KBC set targets for 2028, including a compound annual growth rate (CAGR) of at least 7.7% for total income from 2025-2028, and a further improvement in the cost-income ratio to below 38%.

The guidance reflects KBC’s confidence in its business model and strategic direction, as well as its ability to continue generating sustainable growth. The bank’s planned acquisitions, including 365.bank and Business Lease, are expected to contribute significantly to future profit and loss, with an aggregate projected contribution of €261 million to total income in 2026, growing to €297 million by 2028.

KBC also announced a proposed total dividend of €5.10 per share for FY 2025, maintaining its commitment to shareholder returns while preserving a strong capital position.

In conclusion, KBC Group’s Q4 and FY 2025 presentation portrays a company executing effectively on its strategic priorities, delivering strong financial results, and positioning itself for continued growth. The bank’s integrated model, digital transformation, and disciplined cost management have created a solid foundation for future performance in an evolving financial services landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.